jbk_photography/iStock Editorial via Getty Images

Mastercard (NYSE:MA), with a market cap over $350 billion, is one of the main international credit card companies. I recently wrote an article on Visa (V), another credit card giant. I like the business model of both companies, as it generates very high margins, but the valuations are too high to consider buying either company today. Investors that follow Berkshire Hathaway’s (BRK.A) (BRK.B) 13-F filings should be aware that Warren Buffett trimmed both the Visa and Mastercard positions in Q3.

Investment Thesis

Mastercard’s business is one of the best in the world. As a key part of the world’s current financial transaction system, they have huge operating and net income margins. I would love to own shares of Mastercard, but I wouldn’t pay more than 30x earnings for a mature business the size of Mastercard. They operate a quality business, but the valuation premium is too steep at current prices. In the coming years, the world’s financial system also faces a significant amount of uncertainty, with the explosive growth of smaller fintech companies and cryptocurrencies.

The Business

Mastercard’s business is a proven cash cow. Their revenue primarily consists of service and cross border transaction fees. With operating margins at 53% and net margins at 46%, a huge chunk of revenue flows to the bottom line. As I mentioned in my article on Visa, Mastercard’s margins, while impressive, are still slightly lower than Visa’s.

Mastercard still has plenty of money to reward shareholders with increasing dividends and buybacks. The dividend growth has been impressive, and the current payout ratio is very safe, but what would frustrate me if I were a long-term shareholder is the buyback program.

Buybacks

Mastercard, like so many other large public companies, has been buying back stock as fast as possible. In the first nine months of 2021, the company repurchased $4.6B worth of stock at an average price just over $360. There is $5.2B remaining on the current buyback program. This is where I have a bone to pick with management.

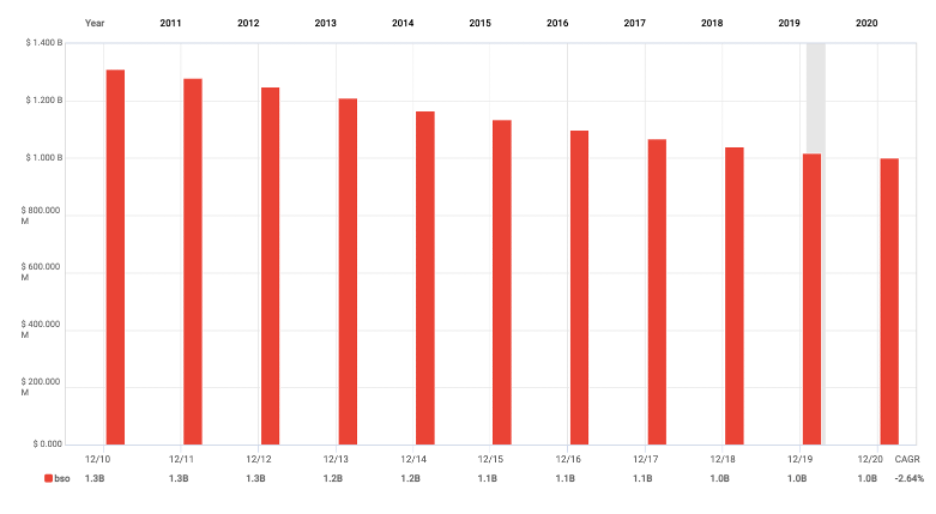

Shares Outstanding

fastgraphs.com

In my opinion, management has been flushing shareholders’ money down the toilet with the buybacks, especially over the last 5 or 6 years as the valuation continued to get richer and richer. I have nothing against buybacks, and when they are done at attractive valuations, I celebrate them. However, when a company is buying back shares at 40-50x earnings, like Mastercard has been doing in the first nine months of 2021, I don’t think long term shareholders actually benefit. This takes us to the most important reason to avoid shares of Mastercard at the current prices: valuation.

Valuation

Investment risk comes primarily from too-high prices, and too-high prices often come from excessive optimism and inadequate skepticism and risk aversion. – Howard Marks

The great thing about investing is that there are plenty of giants whose shoulders you can stand on. Each investor can pick and choose who they want to listen to, who they want to quote, and who they want to ignore. Howard Marks, the founder of Oaktree Capital Management, might be more focused on credit instead of equity, but his quotes are often spot on when it comes to his overall takes on the market.

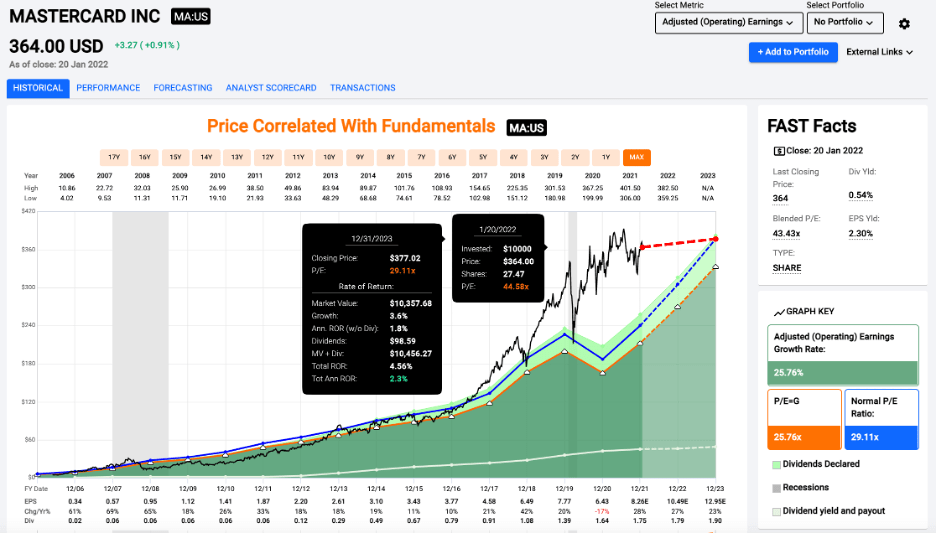

When it comes to Mastercard, I fail to see how 44.5x earnings is attractive for a company that is worth more than $350B. I’m not against paying higher multiples for a small, high-quality business growing rapidly, but as a business gets larger and larger, I get more reluctant to pay a premium multiple. Mastercard’s normal multiple over the last 15 years has been just over 29x earnings, and I think investors who have owned shares for a long time should consider taking some chips off the table.

P/E

fastgraphs.com

To be perfectly honest, I don’t think Mastercard is worth the $354B market cap. Could it be worth that amount in the future? Sure, but it will take a couple years of significant business growth to make it happen. Mastercard could continue to see attractive returns if the multiple continues to expand, but I find that scenario highly unlikely.

Conclusion

Mastercard is a fantastic business. No ifs, ands, or buts about it. The company has been printing money for a long time and that pattern will likely continue. So, while I won’t be buying shares, I’m not bearish, even with the premium valuation. Investors holding Mastercard at current prices probably won’t get wiped out, but the forward returns don’t look that attractive to me. Investors who have owned Mastercard for a long time should decide for themselves if it’s time to take some gains and reinvest elsewhere.

I would be fascinated to hear your thoughts. Feel free to leave a comment below.

from WordPress https://ift.tt/3rGAumb

via IFTTT

No comments:

Post a Comment