EyeOfPaul/iStock Editorial via Getty Images

Dear Readers/Followers,

To those of you following my work, it should be very clear that I’m largely the opposite of someone in my age group (30-35-ish) in how I invest. I don’t invest heavily in tech (less than 2%), I’m extremely conservative and traditional in my approach. I don’t consider investments in things such as Bitcoin, NFTs, or what I view as highly speculative “something’s” as interesting to me.

This isn’t to say that these things might not have an upside for you – but when you read my things, you can always assume that my stance will be this, for as long as I view the fundamentals in these things as incalculable and uninteresting for my investment goals and risk tolerance.

I like yield, and I like a conservative approach.

So, let’s look at UBS (UBS).

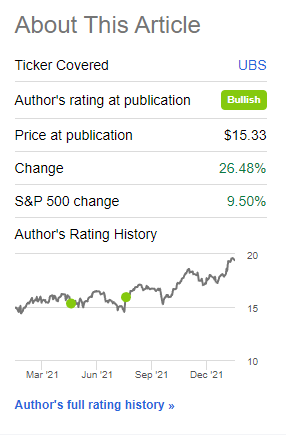

Since my first article on SA, the company has done this.

Seeking Alpha UBS article

People don’t like UBS – but I find that people often don’t like math and facts – and to me, UBS was an investment of “math and facts” back about half a year or so ago.

UBS Logo

UBS Corporate

Revisiting UBS

UBS is the largest Swiss bank on earth. Its headquartered in Zürich, in offices that, less the glass doors, look like something out of Game of Thrones, and maintain a strong presence in all major financial centers on earth.

UBS Headquarters

It’s the largest private banking institution in the world. They cater to a significant portion of the world’s billionaires as their clients, and as of 2021, it’s also the 3rd-largest bank in Europe thanks to their market cap – in no small part thanks to exactly these billionaires.

It has over 3.2 trillion Swiss francs in AUM, with 2.8 trillion invested in assets. It has the highest RoiC in its peer group, at over 11.1%, with others, including US majors such as Goldman (GS) and JPMorgan (JPM) averaging under 10%.

Despite all of the scandals rocking this bank, UBS averages an A- credit rating, making it one of the best-rated banks in Europe. It has sufficient CET-1 ratios and some of the best RoEs in the entire business with over 15%.

The aforementioned secrecy for its clients of course results in an untold level of brand loyalty from its wealthy clients. 50% of all the billionaires in the world are clients of UBS, which I view as an argument for investing in the bank in itself. If you’re building wealth, associate or side with the people that have already built wealth.

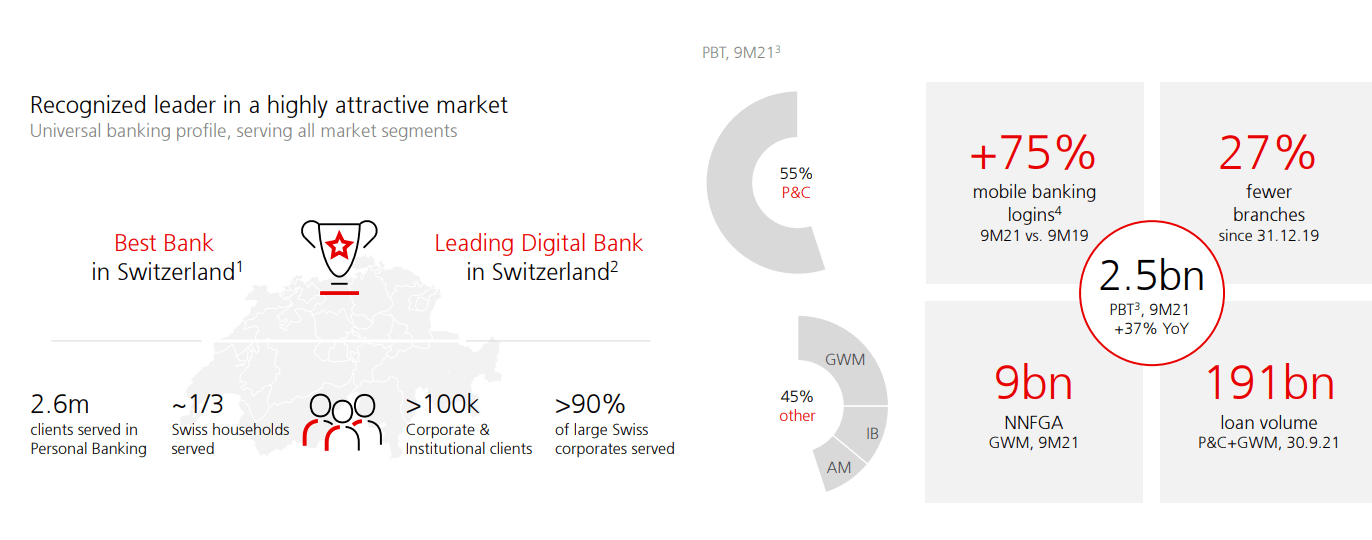

UBS 3Q21 Presentation

UBS 3Q21 Presentation

Moving into recent results. In 2021, the company has been substantially increasing its business volume. Global banking income is up 44%, with 200 billion CHF of newly invested assets YoY on 9M21, as well as over 21b in new loans – more loan volume in 9M21 than the entire revenue for certain peer banks. Its CET1-ratio improved to nearly 15%, and return on capital is at an all-time high, at 20.8% for 3Q21.

It’s also, by far, the leading and “best” bank in Switzerland on a national level.

UBS 3Q21 presentation

UBS 3Q21 presentation

Every single important metric is up as of 9M21. Net profit is up, pre-tax profit is up, EPS is up, RoE is up, and segments are showing record business, including Global Wealth Management, with other segments recording excellent overall business levels, even if they’re not at all-time highs.

Following the financial crisis as the substantial losses seen for UBS, the bank made the very clear decision to more or less cut its investment banking business to the bone. This was substantially different from some of its peers, including Credit Suisse (CS) and Deutsche Bank (DB).

We have to realize just how significant losses were back then to see why the bank acted like this. Losses led to equity attributable to shareholders decreasing by 68% back in 2008, which were to bring 3 loss-making years, which were only broken after 2010.

For the analyst in me, the company has simplified its operations by opening three banking subsidiaries in the UK, Switzerland, and the US. This means that when analyzing, we can look at reported actual figures as opposed to adjusted ones – a welcome change to be sure. The company has also been putting a greater weight towards share buybacks as opposed to earlier, with an FY20 dividend of only 0.37 CHF, lowering it by around 50% YoY. The current set of expectations does not forecast UBS to raise the dividend more than token a centime/cent on an annual basis.

This needs to be taken into consideration prior to investing. UBS might be one of the best banks, but it’s not a high-yielder – nor is it likely to become one with a very recent dividend goal restatement.

Bank issues (Penalties)

On a high level, UBS is a wealth manager.

What causes me to say this is that more than half of the company’s annual revenues of around 32-35 billion francs come from wealth management, and almost 50% of that is from private banking alone. It truly is a billionaire’s bank, and the Global Wealth Management arm is the crowning glory of this company.

If you invest in UBS, you should view such trends and billionaire banking as favorable.

The bank’s core business is this wealth management, which comes at a very high profit margin, contributing more than 50% of the company’s pre-tax profits.

The legacy/retail banking operations are neither a net positive nor negative to me – it’s simply something the bank does, and they’re good at it. In my view, the removal of IB altogether would serve UBS the best and allow it to focus on these things.

Aside from IB and the risk it contains, there are a few developments worth mentioning for UBS that merit investor consideration.

In 2019, a French court decided that UBS would pay a penalty due to Tax Fraud allegations in helping French wealthy clients avoid tax payments. UBS has already appealed this (effectively suspending the decision), and this penalty was reduced to €1.8B a few weeks back. UBS has not yet decided whether to appeal. (Source: Reuters)

The crux here is that the FY20 balance sheet from an accounting perspective did not sufficiently provision for a penalty of €1.8B, but only for €450M. This reflects a difference between what could be needed, and should therefore be included.

As the last item, the bank has downgraded its expectation for future period returns to around 12-15% for 2020-2022. The bank has already exceeded this for 2021, but it’s healthy to forecast a lower growth rate here. The company is targeting 10-15% annual RoR for its GWM business, and lower for Investment banking. (Source: UBS IR)

While these risks exist, UBS has been a clear winner of COVID-19, and surprisingly enough, its investment banking arm, which was able to recognize disposal gains of over $600M because of a sale. Also, its targets were significantly beaten during 9M20, as well as this year. Any COVID-19 impact has been comparatively minimal. While this has been a trend for many European and global banks, UBS is a great example of this overall.

How to view and value UBS

This is an interesting business and bank to try and value.

The only valuation-related area where UBS falls short of peers and other banks is the company’s very modest, now-cut yield at under 4%. In my view, solid banks should be high dividend payors. UBS is no longer that. This impacts my view, and I’m assigning a bit of a discount because of it.

The GWM and asset management are easy to value – we use AUM, and weigh other divisions on the basis of 2021-2025 average weighted forecasts on a pre-tax basis.

Peers include all other European banks to some degree. It includes Swedbank (OTCPK:SWDBF) (OTCPK:SWDBY), Handelsbanken (OTCPK:SVNLF) (OTCPK:SVNLY), Nordea (OTCPK:NRDBY) (OTCPK:NBNKF), Deutsche, Credit Suisse, BNP Paribas (OTCQX:BNPQF) (OTCQX:BNPQY) (OTCPK:BNPZY), and local peers like Julius Baer (OTCPK:JBAXY).

That UBS following the banks 2021 is undervalued is based on one simple thing – a premium.

If you’re willing to assign a 10-20% premium, reflecting UBS’s smaller focus in IB and its massive position as well as its billionaire appeal (all of which I view as relevant), that’s when the company really shines out in terms of valuation to its peers.

If you don’t apply this sort of premium, especially to its yield, which now is at a sub-3% level, then UBS quickly starts failing on a yield and a P/E as well as a book basis. It was more undervalued before it appreciated, but today’s share price essentially requires you to give it that solid premium.

Most analysts/sources do.

Even at a current level of 17.75 CHF/share for the native, analysts bring an average target of 19.75 (Source: S&P Global) for the company, with equity analysts pretty much landing on the same level at 19.6 CHF. (Source: AlphaValue)

Where I differ from these analysts is that I place a greater weight on the bank’s dividend yield and comps, where UBS really suffers, and don’t agree on the size of the premia that are being applied to UBS. This leads me to a lower share price target of around 18.3 CHF/share.

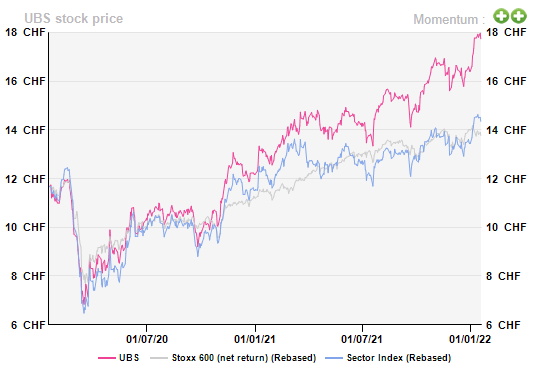

UBS has outperformed the market – as has my position in the bank, appreciating more than 30% on a 1-year basis.

UBS Stock performance

I will say that if UBS were to keep its company targets of 10-15% average annual profit growth for the next few years, then the stock is most certainly a “BUY” here, even at a relatively low upside. The fundamentals of UBS, coupled with its client appeal is a big one to me. UBS isn’t going anywhere.

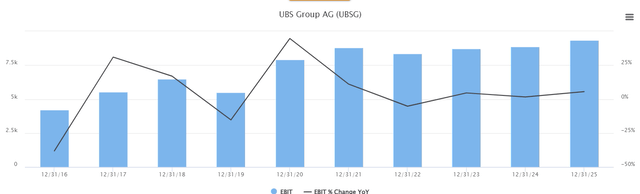

Current equity analysts’ forecast call for this. S&P Global is targeting the lower end towards this spectrum at around 9.8% forward until 2025.

UBS EBIT growth

What can be said is that following the financial crisis and the group’s reorg from IB, things have gone very well for UBS. I believe this trend is likely to continue even with the current lower potential returns for the coming 1-3 years, and that’s why I agree with the overall view that UBS is likely to bring about at least 9-11% annual pre-tax profit increases.

Even if this is not a “dividend bank”, with the 2024E dividend essentially indicating a ~2.5% yield here (Source: S&P Global, AlphaValue, FactSet), it’s a part of my portfolio that I have no intention of changing at this valuation. I’ve already made well over 30%, outperforming doubters as well as the market.

And I expect more out of UBS.

Concluding UBS

Why is that? Why am I so positive here?

Simple.

The power of capital. UBS handles 50% of the world’s billionaires as well as large portions of their funds. What UBS can do with this capital and the returns it offers has already been exemplified throughout COVID-19 and during the last couple of years. The company bought back more in stocks than most banks have in revenue in a single year. The company paid more in shareholder dividends than most smaller banks are valued in terms of market cap.

The power of capital. UBS was not only somewhat correct, but they were also in my view 100% correct to wind down IB, and focus on becoming the world’s best “billionaire bank”.

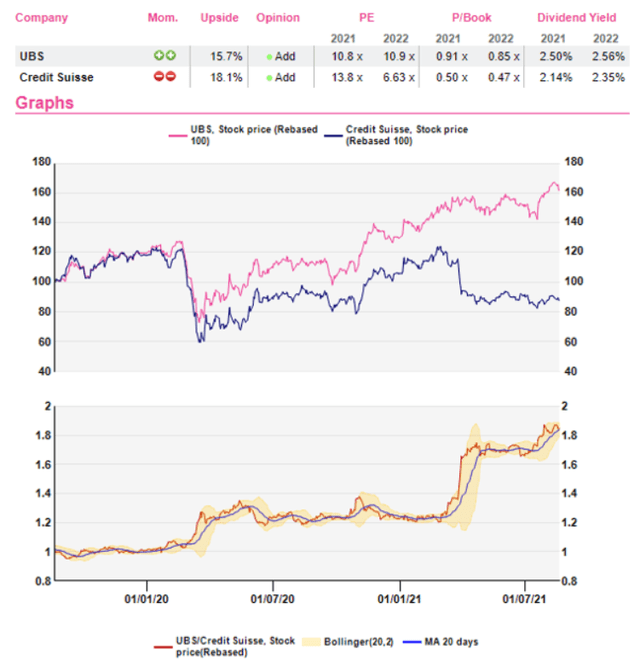

The demise of close peer Credit Suisse on a compared note can be seen as proof of this.

AlphaValue, UBS/CS

Is it perfect yet? No – still has some work to do, for sure. But at current levels, UBS is an appealing bank simply for the reason of its clientele and income profile. Much of it is fee-driven, which saves it from interest rate dependency to some extent, and while any bank will be hurt in a downturn, UBS is one of the safer ones that I see.

This is a heavily content-reduced article of one that was published on iREIT on Alpha on Wednesday the 19th of January. The original piece delves deeper into risks, valuation, and the core thesis in the context of the bank’s peers. It doesn’t change the ending target, but it gives you a better understanding of the context and considerations you should take prior to investing.

This one is a “BUY” as well as a “HOLD”, dear subscribers. I’m buying to hold, and would only sell it at a high premium given its specifics. This stock is also part of AlphaValue’s “Buy and Hold list”, and while my core portfolio has outperformed the analysts’ lists by a factor of nearly 6% for 2021, as well as nearly 13% for 2022 YTD (Source: AlphaValue, measured returns for B&H portfolio, Author’s Calculations), I still view many of their picks as very good.

This is one of them.

UBS is a “BUY” with a price target of no less than $21 for the long term.

from WordPress https://ift.tt/3nNUDFS

via IFTTT

No comments:

Post a Comment