robertcicchetti/iStock Editorial via Getty Images

Investment Thesis

Sellers continue to take control of ChargePoint Holdings’ (CHPT) stock performance. The stock has also breached a critical support level that it has firmly held since it completed its SPAC combination in February’21. As a company still early in its EV charging market opportunity, it also garnered huge interest among investors. Nevertheless, the significant correction in high-growth plays has also impacted CHPT stock. Given its focus on growth over profitability, investors continued to bail out for proven quality.

However, the secular drivers underpinning the EV charging leaders remain intact. Moreover, even though the automakers are keen to operate and monetize their own charging infrastructure, they can’t do this alone, given the size of the EV TAM. Therefore, we believe that there are potential opportunities for leaders like ChargePoint to leverage if they can execute well moving forward.

We also issued two Neutral calls previously on CHPT stock as we considered it too pricey then. Since those articles were published, it has declined 46% and 27% (appended here and here), respectively. Consequently, the stock is now very close to our implied fair value (+/- 10%). Therefore, we are prepared to upgrade it to Buy, based on a marked improvement in its risk/reward profile. We discuss more below.

ChargePoint Is Focusing On Its Higher-Margin SaaS Business

ChargePoint has telegraphed its plans clearly from the start that it sees itself as a SaaS-focused company. The company doesn’t operate charging infrastructure, but it sells its charging systems to its customers and attaches them with its recurring subscription-based SaaS model. The focus on SaaS is clear because of its much higher margin profile.

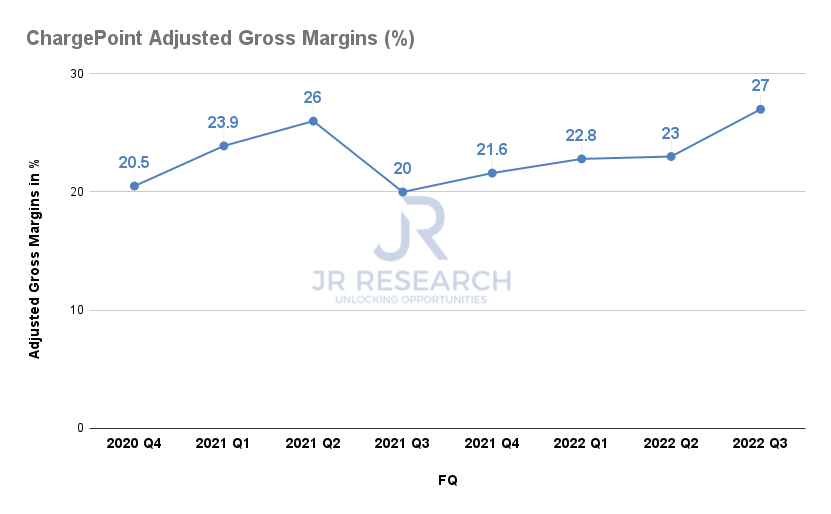

ChargePoint Adj. gross margins

Company filings

The company reported an adjusted gross margin of 27% in FQ3’22, but its subscriptions gross margin was 41.9% on a GAAP basis and about 50%+ on an adjusted basis. Nevertheless, it’s important to note that even when we consider CHPT’s adjusted gross margin for its subscriptions, it’s still discernibly low. It’s an inherent characteristic of ChargePoint’s business model, where it recognizes network fees and depreciation & amortization charges in its gross margins. Given that it also runs CPaaS arrangements, it’s challenging to expect the high SaaS gross margins we have been used to, to be fair.

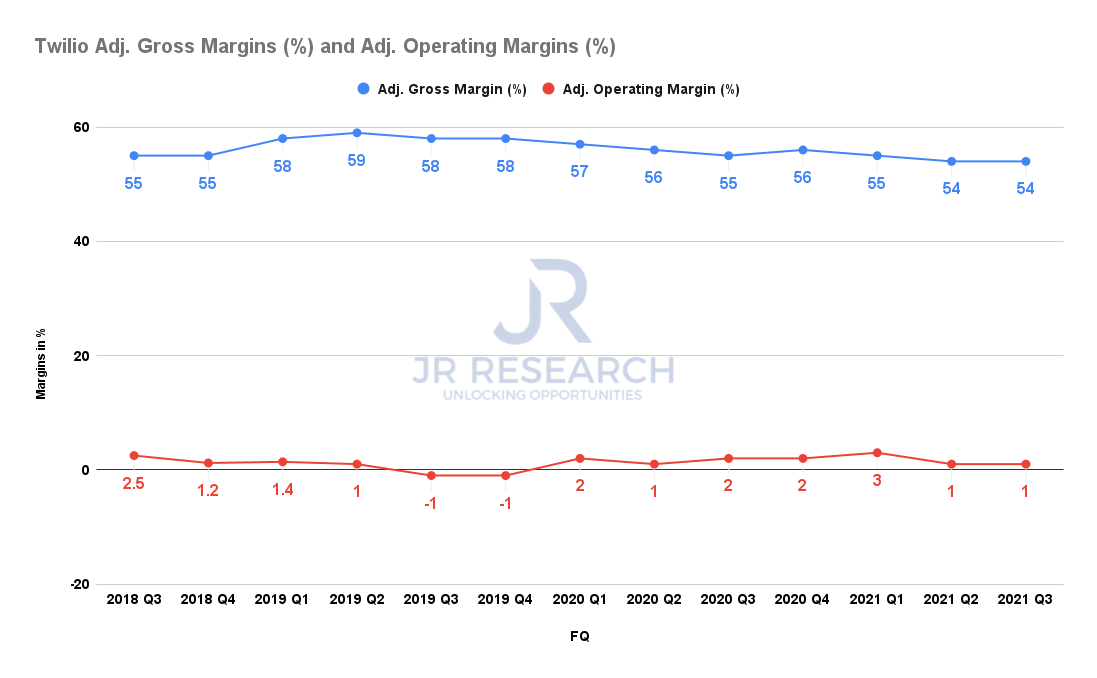

Twilio Adj. gross margins

Company filings

Although not directly related, CPaaS leader Twilio’s (TWLO) adjusted gross margins are also in the 50s. Therefore, network fees and their related charges would impinge on CHPT moving towards the type of SaaS margins that SaaS investors have been used to.

As a result, we highlighted in our previous article that investors must be cautious when ascribing revenue multiples they used to value high-growth SaaS stocks. We don’t think CHPT stock deserves such premium multiples due to its inherently weaker margins profile.

Despite that, we believe that ChargePoint still has the potential to improve its SaaS margins. One thing for sure is that the EV penetration rate in the US is just over 4% in 2021 (up from just 2% in 2020). Credit Suisse expects the momentum to continue as it estimates that EV share of sales in the US could reach 8% this year and up to 50% by 2030. While the forecast seems aggressive, the US EV momentum outperformed estimates released by BloombergNEF back in June’21. It had expected EV share of sales in the US to reach just 3.5% in 2021. Furthermore, famed Wedbush tech analyst Dan Ives also expects the “green tidal wave” to lift the leading EV players towards a massive $5T global opportunity. Moreover, ChargePoint is also penetrating further into Europe, where the EV momentum has continued to gain traction in 2021. Schmidt Automotive Research highlighted that Europe’s BEV momentum had improved further in 2021. BEV share of sales in Western Europe topped 11% on average in 2021 and also reached 20% in December. Moreover, ChargePoint is already operating in 16 European markets. We believe that it’s an astute move given Europe’s faster and more forthcoming adoption of EVs.

Notably, ChargePoint aims for its European business to account for 1/3 of its total revenue. ChargePoint believes that its network compatibility in Europe can help drive adoption faster and underpin its growth momentum there. CEO Pasquale Romano emphasized (edited):

We have a lot of third-party hardware on our network. It’s pretty unmatched with respect to compatibility with the plethora of hardware present. And that’s how it moves us up the curve, We’ve certainly moved up the curve quite a bit on a port count basis. Most importantly, it’s an all-software business there. So all of that business is of the high-margin software type. We can also sell hardware into that customer base now that we are a joint company. (24th Annual Needham Growth Conference)

Its Valuation Has Improved Markedly

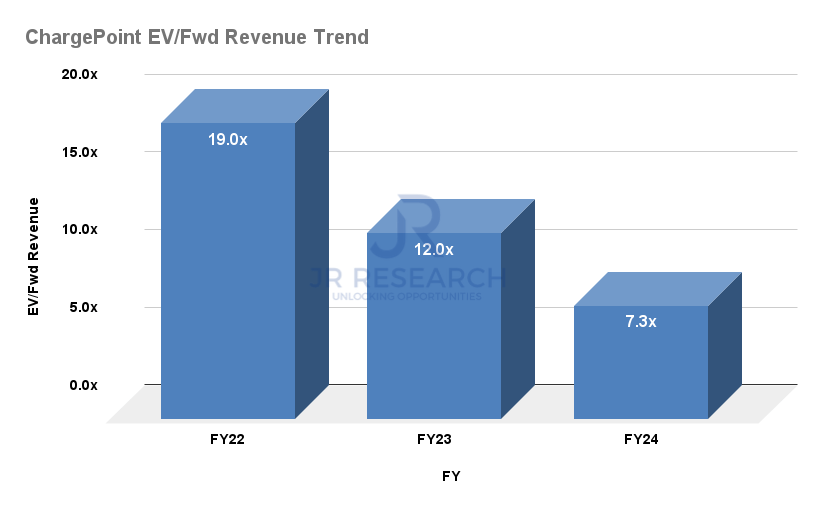

ChargePoint stock EV/Fwd Revenue Valuation

S&P Capital IQ

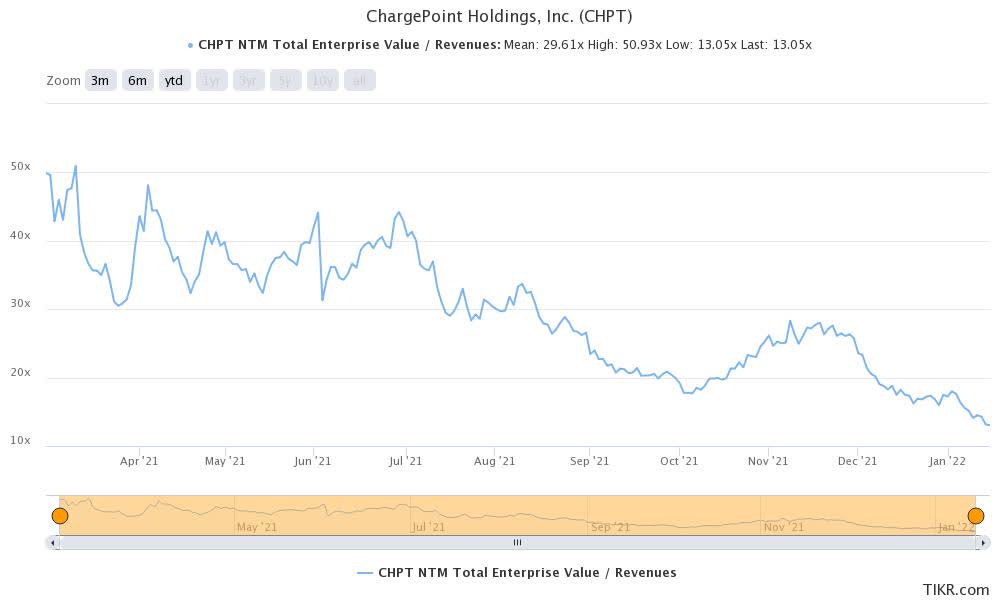

ChargePoint stock EV/NTM Revenue trend

TIKR

As explained earlier, readers can easily glean that ChargePoint stock’s valuation has fallen dramatically. It’s now trading at 13x NTM revenue due to the battering. Nevertheless, we still think it looks pricey if we consider its high-growth SaaS peers median multiple of 15.2x. But, at least it’s much lower than the 27.3x that it traded at when we first covered it in November. Hence, we believe that its risk/reward profile has improved remarkably.

Moreover, the company is still expected to grow its topline rapidly. Consensus estimates point to a revenue CAGR of 61.9% from FY21-24. In addition, it’s also expected to gain operating leverage as it scales.

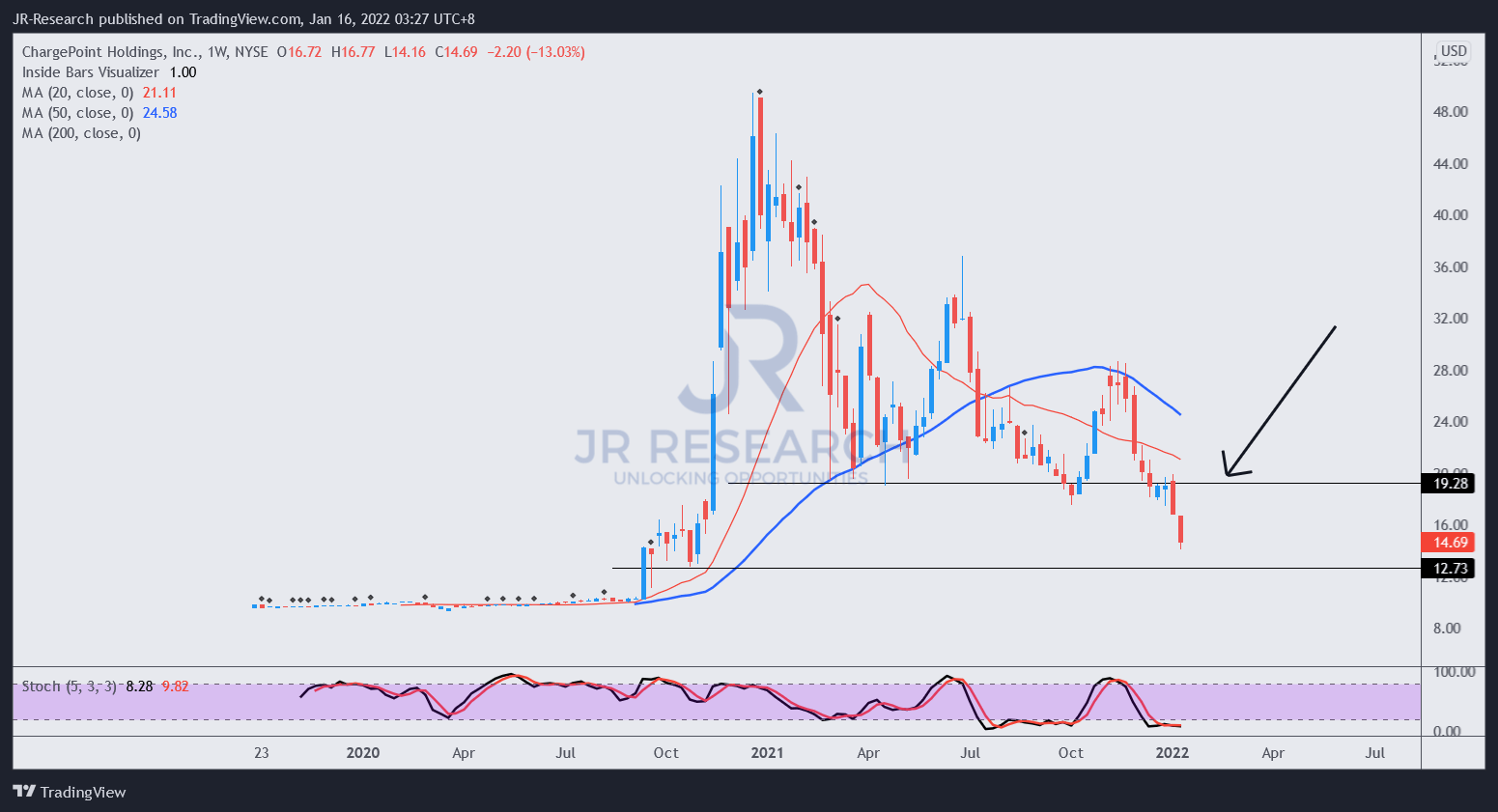

CHPT stock price action

Tradingview

Nevertheless, we must highlight that the stock’s momentum is extremely weak. In addition, it has also broken down below its key support level of $19, as shown above. That level has supported the stock since it completed its SPAC combination. Therefore, the initiative is definitely with the sellers right now. As a result, we believe that there’s a possibility for the stock to decline further to $12.70 (about 13.5% below its last closed price). But, our thesis is not based on a swing trading framework, so we are not unduly concerned. We wanted to highlight the potential for continued volatility if you decide to add at the current level. Perhaps, you can space out your allocation to average down if it drops further.

Nonetheless, as discussed above, we are confident that the stock’s risk/reward profile has improved markedly. Consequently, we revise our rating on CHPT stock from Neutral to Buy.

from WordPress https://ift.tt/3rsata2

via IFTTT

No comments:

Post a Comment